Everything we've covered so far — trading, algorithms, day trading, swing trades — is about generating alpha on shorter timeframes. But there's another side, and for most people, it's where the real wealth gets built.

Long-term investing. Buying exceptional assets at reasonable times and holding them for years, sometimes decades, while compounding does the heavy lifting. It sounds boring. It is boring. That's the point. The most powerful wealth-building force in financial history doesn't require cleverness, speed, or sophisticated tools. It requires patience, discipline, and a framework.

Started putting £400 per month into a broad index when he was 23. Didn't pick stocks. Didn't try to time the market. Didn't even look at his account more than twice a year.

By 38 — fifteen years in — his portfolio was worth around £180,000. He'd contributed £72,000 of his own money. The rest was compounding. By the time he was 50, he was a millionaire. Not from one brilliant trade. From patience.

Why Long-Term Investors Underperform

The average investor's returns are shockingly bad compared to the markets they invest in. Over the twenty years ending in 2023, the broad stock market returned approximately 10% per year. The average equity fund investor earned approximately 6%. The gap — roughly 4% annually — is enormous over time.

Where does the 4% go? It's destroyed by investor behaviour. People buy after the market has already risen (chasing performance), sell after it has already fallen (panic), tinker with their portfolios too often (generating taxes and fees), and make emotional decisions at exactly the moments when emotional decisions are most costly.

Missing the ten best days in the market over a twenty-year period cuts your total return roughly in half. And those best days happen almost always during or immediately after crashes.

In April 2020, he told me he'd sold his entire portfolio on March 18th — three days before the absolute bottom. He'd been investing for twelve years. Had a beautiful portfolio of quality companies.

When I asked why he sold, he said: "The losses were too big. I couldn't watch anymore. I told myself I'd buy back when things calmed down." Things calmed down exactly one week later. The market rallied 70% over the next year. He never bought back.

This is why you need a framework. Not opinions. Not gut feelings. Not what the news is saying. A framework that tells you what to buy, when to buy it, and under what conditions to sell. Decisions made in advance, with a clear head, before the next crash arrives.

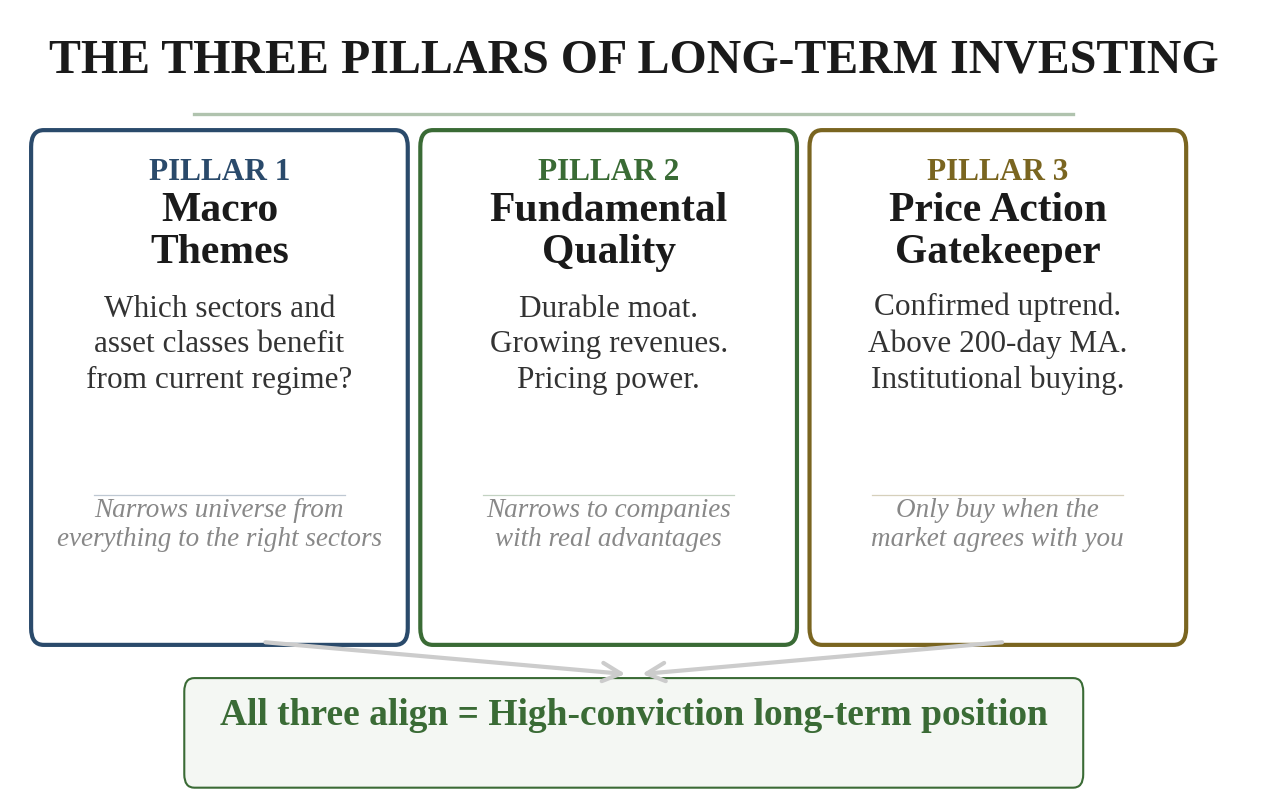

Pillar One: Macro Themes First

Instead of asking "What regime are we in this month?" you're asking "What are the dominant economic forces of the next five to ten years, and which sectors and asset classes will they favour?"

Identify the structural tailwinds and position your long-term capital to benefit from them. When you're investing for decades, getting the macro theme right matters far more than getting the entry price perfect.

In the decade following 2010, the dominant themes were near-zero interest rates, low inflation, globalisation, and the rise of digital technology. If you understood those themes, the implications were straightforward: technology stocks, growth companies, and long-duration assets.

From 2020 to 2025, the themes shifted dramatically: inflation returned, interest rates rose, supply chains restructured, energy security became a priority, and artificial intelligence emerged as a transformative technology. The winners changed accordingly.

The point isn't to predict the future with precision. It's to identify the structural tailwinds. Buying the right sector at a mediocre price is far more profitable than buying the wrong sector at a perfect price.

Pillar Two: Fundamental Quality

Once you've identified which sectors to focus on, select individual holdings based on quality. Because you're holding for years, a mediocre company can deliver a profitable trade over two weeks. Over five years, that same mediocre company will disappoint you.

Four characteristics define a company worth owning for the long term:

Durable competitive advantage. A network effect, cost advantage, switching costs, or brand power that competitors cannot easily replicate. Something that keeps customers coming back and keeps competitors out.

Consistent profitability. Reliable operating margins, stable or growing return on equity, and free cash flow that doesn't depend on favourable market conditions. A company earning 15% ROE in good years and 5% in bad years is better than one earning 25% and then -10%.

Robust balance sheet. Manageable debt relative to earnings and cash flow. Companies with strong balance sheets survive recessions and often emerge stronger, acquiring weakened competitors at distressed prices.

Sustainable growth potential. A credible pathway to growing revenue and earnings over five to ten years. Not outsized hyper-growth — realistic, fundable expansion.

The Moat Erosion Trap

Network effects can be disrupted by new platforms. Cost advantages can be eliminated by technology. Brand loyalty can evaporate when a better product arrives. The moat that made a company great in 2015 might be half-full by 2025.

Review your holdings constantly, but act patiently. Watch for declining margins, losing market share, management making excuses instead of changes.

Specific red flags to watch for:

Operating margins declining for three consecutive quarters without a clear, temporary cause

Revenue growth decelerating to below industry average for two or more quarters

Key management departures, especially in product or technology leadership

Increasing reliance on acquisitions rather than organic growth

Competitors gaining market share while the company's narrative shifts from growth to "efficiency"

Pillar Three: Price Action as Gatekeeper

This is where this book diverges from almost every other investing guide. Most will tell you that if fundamentals are great, buy regardless of price action. This book disagrees. A stock in a sustained downtrend is telling you something. Maybe the market knows something you don't.

Never commit significant long-term capital to an asset in a confirmed downtrend. Wait for the trend to stabilise and begin turning upward before building a position.

The stock should be above its 200-day moving average, the moving average should be sloping upward or flattening, and recent price action should show signs of accumulation — higher lows, increasing volume on up days.

When to Enter Long-Term Positions

The ideal entry is during a pullback within a confirmed uptrend. The stock has been making higher highs and higher lows. The macro theme supports it. The fundamentals are solid. Then it pulls back 5–10% on normal profit-taking. That's your entry window.

The second-best entry is at the beginning of a new uptrend. The stock breaks above its 200-day moving average for the first time in months, on above-average volume. The fundamental story is intact. The macro theme has shifted in its favour. This is a "regime change" entry.

What you never do is buy into a sustained downtrend because the stock "looks cheap." A stock at £50 that was £100 six months ago isn't cheap. It might be expensive if it's heading to £25.

When to Exit Long-Term Positions

The moat is eroding. Margins compressing. Revenue stalled. The thesis that justified your purchase is no longer intact. This isn't a one-quarter blip — it's a pattern.

The stock breaks below its long-term moving average on heavy volume and fails to recover. Lower highs and lower lows establish a downtrend. The price action gatekeeper is telling you the market has changed its mind.

The regime moves to an environment that historically punishes the sector you're in. Doesn't always mean selling immediately — but it does mean heightened vigilance and reduced position size.

A new opportunity emerges with dramatically better risk-adjusted returns — a different sector entering a supportive regime with strong fundamentals and a confirmed uptrend. Capital is finite. Rotate when the evidence is clear.

The one thing you never do is sell because the price dropped 10% in a week during a broad market correction. If fundamentals are intact, the macro theme is intact, and the trend is still structurally upward, a drawdown within an uptrend is an opportunity to add — not a reason to panic.

Putting the Three Pillars Together

The three pillars work as a filtering system. Pillar One narrows from every asset in the world to 3–5 favoured sectors. Pillar Two narrows to 10–20 quality names. Pillar Three narrows to the 3–8 positions in confirmed uptrends right now.

That's your long-term portfolio. Three to eight high-conviction positions in fundamentally excellent companies, in macro-supported sectors, in confirmed uptrends. Concentrated enough to generate meaningful returns. Diversified enough that no single position can destroy you. Our market products cover equities alongside five other markets, all graded through this same framework.

The best long-term investors look lazy from the outside. They're not lazy. They're disciplined enough to do nothing when nothing needs doing.

Review constantly. Act patiently. Most months, you do nothing. The positions are working. The compounding is compounding. Your job is to let it happen and only intervene when the data demands it. See what patient, conviction-based trading delivers on our verified track record.

The next chapter covers the specific mechanics of dollar-cost averaging, lifecycle investing, and building the multi-pillar portfolio structure that balances growth, income, and speculation.

- 1.Macro themes first — getting the sector right matters more than getting the entry price perfect over a multi-year horizon.

- 2.Fundamental quality (moat, profitability, balance sheet, growth) determines which companies are worth holding for years.

- 3.Price action is the final gatekeeper — never commit long-term capital to an asset in a confirmed downtrend.

This content is for educational purposes only and does not constitute investment advice. Trading and investing involve substantial risk of loss. Past performance is not indicative of future results. Always do your own research and consider seeking professional guidance before making financial decisions.