Here's a thought experiment that will change how you think about your money.

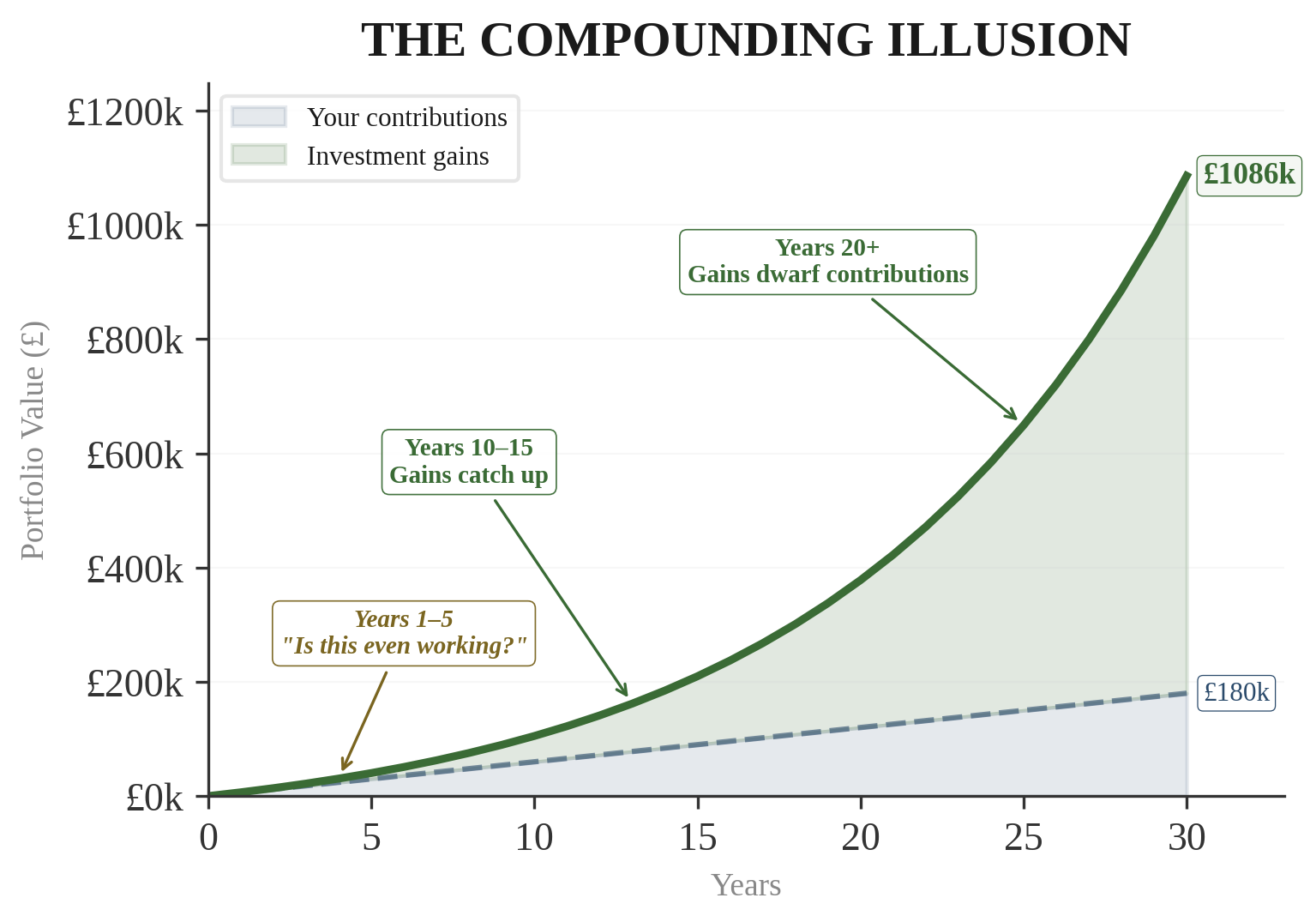

Imagine two versions of you. Version A starts investing at age 25, putting £500 per month into a broad stock market index fund, and stops contributing at 35. Ten years, then nothing. Version B starts at 35, contributes the same £500 per month, and keeps going for thirty years until 65.

The ten-year head start was worth more than twenty additional years of contributions. This isn't a trick. It's the mathematics of compounding. Time is your biggest edge — bigger than stock picking, bigger than market timing, bigger than any strategy in this book. And unlike every other edge, this one doesn't require skill, knowledge, or luck. It only requires starting.

Every year you delay investing costs more than the last. Not because the market changes, but because compounding accelerates with time.

The Retirement Paradox

Consider someone who is 25 with £10,000 to invest. If the market drops 50% tomorrow, they lose £5,000. Painful, but survivable. They have forty years of working income ahead.

Now consider that same person at 55, with £500,000. A 50% drop wipes out £250,000. That's years of retirement income. It might be unrecoverable with only ten years of earning potential left.

Conventional advice says take more risk when young (small portfolio, long horizon) and less risk when older (large portfolio, short horizon). But in practice, most people end up with far more money at risk near retirement than at any other point in their lives — because the portfolio itself has grown.

Your biggest market exposure happens at the worst possible time — right before you need the money.

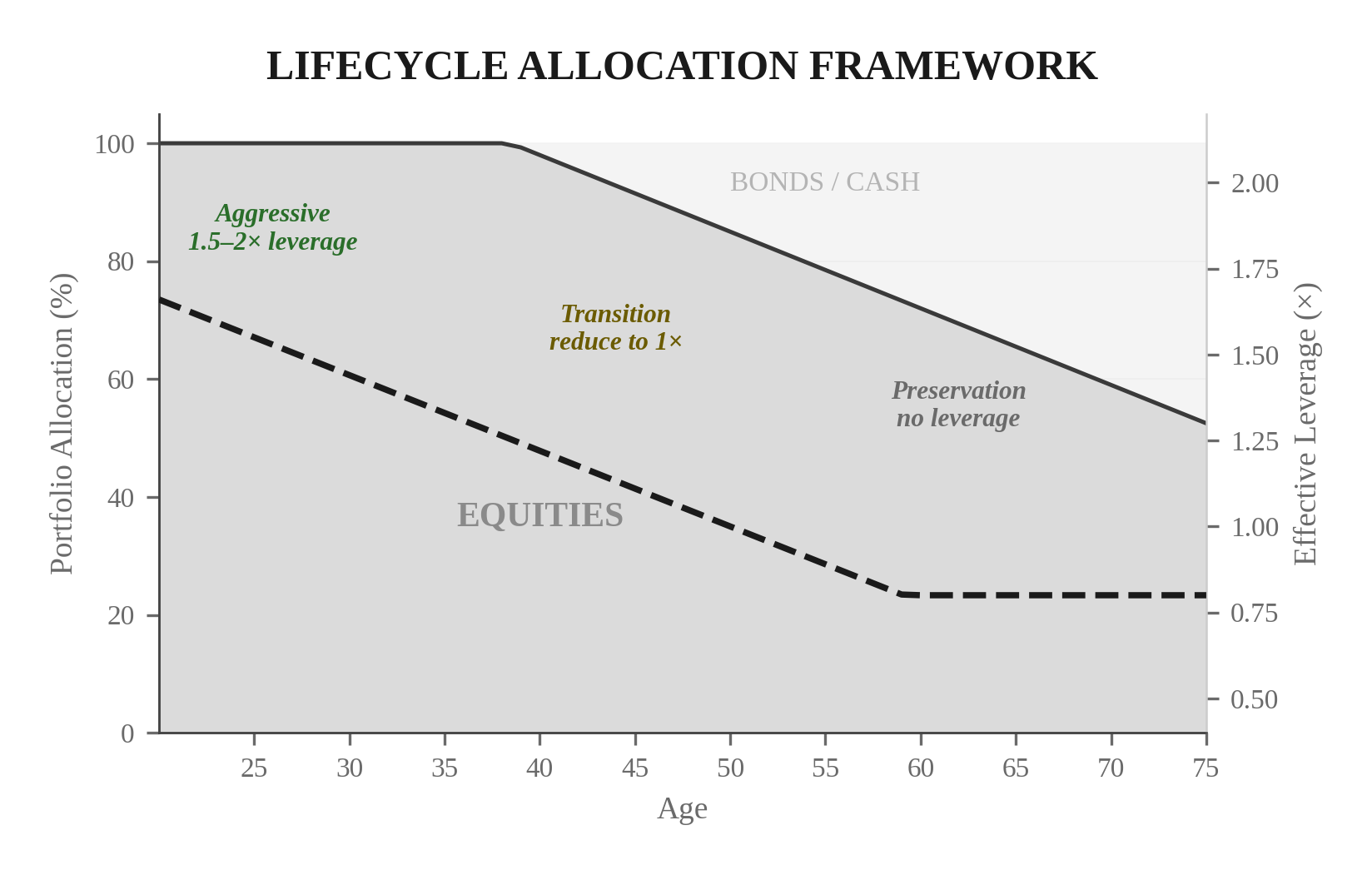

The Lifecycle Investing Framework

This is one of the most important ideas in this entire book. Instead of gradually increasing your total stock market exposure over time, you should aim for roughly consistent exposure across your entire investing lifetime. In practice, this means using moderate leverage when young (when your portfolio is small but your human capital is large) and reducing exposure as you age (when your portfolio is large but your human capital is declining).

The Practical Framework

Moderate leverage — 1.5–2x your stock allocation. A 25-year-old with £10,000 at 1.5x has £15,000 of market exposure. If the market drops 33%, they lose £5,000. Painful. Recoverable. The expected return over 30+ years dramatically outweighs the short-term volatility.

Reducing leverage toward 1x as your portfolio grows. The portfolio itself now provides the exposure that leverage was generating earlier. Introduce a meaningful bond allocation for stability.

At or below 1x equity exposure. No leverage. Significant bond allocation. Priority shifts from growth to preservation — but not excessively. You might live to 90. Thirty-five years of inflation will devastate an overly conservative portfolio.

Maintain 50–100% equity depending on circumstances. A 65-year-old with 30% equity has a real problem: their portfolio won't keep pace with inflation over a potential 30-year retirement. Bonds yielding 3–4% minus 3% inflation = treading water.

How to Get Leverage Safely

The word "leverage" frightens people, and for good reason. But there's a difference between reckless 50x leverage on derivatives and moderate 1.5–2x leverage through index funds. The dose makes the poison.

Leveraged index funds: Simplest. A 2x fund gives you £2 of exposure per £1 invested. The downside is internal costs and volatility drag. Best for periods under 5 years.

LEAPS (long-term options): More precise. A deep in-the-money call gives 1.5–2x leverage with a known maximum loss. Cost is explicit and controllable.

Margin accounts: Most direct but most risky. Never exceed 1.5x total exposure. Maintain a cash buffer for margin calls.

The Critical Constraint

Never leverage beyond what you can comfortably handle in a 50% market drawdown.

At 2x leverage, a 50% market drop = 100% loss. You're wiped out. That's not lifecycle investing — that's gambling.

A safer approach: 1.5x leverage with a 20% cash buffer means a 50% decline hits your equity for 75%. Painful. Survivable. And recoverable, because you're young enough to wait.

If the thought of a 50% drawdown on your leveraged position makes you physically uncomfortable, reduce the leverage until you find a level you can genuinely endure without selling.

Don't Become Too Conservative Too Early

People are living longer. A healthy 60-year-old today has a reasonable probability of reaching 90 or beyond. That's a 30-year time horizon. Thirty years. That's as long as a career. And yet, conventional advice for a 60-year-old is to hold 40–60% bonds.

Protecting capital from market volatility isn't the only risk you face. You also face inflation risk — the slow, invisible erosion of purchasing power. At 3% annual inflation, the purchasing power of a fixed income halves in about 24 years. A portfolio heavy in bonds won't keep pace.

Maintaining meaningful equity exposure — 50–80% even in retirement — gives your portfolio the growth it needs to outpace inflation over a multi-decade horizon.

Implementation Tips

Or when major life events change your circumstances. Don't rebalance monthly — the transaction costs and tax implications aren't worth the marginal improvement.

Pensions, ISAs, and equivalent structures should be maximised before taxable accounts. Over thirty years, the tax savings compound just like investment returns — the difference can be 30% or more of your final portfolio.

A broad index fund under 0.10%/year expense ratio. The difference between 0.05% and 1.5% in fees consumes roughly 30% of your total returns over thirty years. Check our verified performance to see how cost-conscious, disciplined investing compounds.

Set up an automatic monthly transfer on payday. Removes willpower from the equation. You can't spend what you've already invested. You can't time the market when the purchase happens automatically. Combine this with our market products for the active portion of your portfolio.

The stock market goes up on roughly 53% of days — nearly a coin flip. Over a month, odds improve to ~60%. Over a year, ~75%. Over ten years, ~95%. The less often you check, the more often you see green.

The next chapter covers the tools and vehicles for long-term investing — options strategies for enhanced returns, and how to combine active trading with passive investing in a unified portfolio.

- 1.Starting 10 years earlier beats contributing 3x more money — compounding accelerates with time, not capital.

- 2.Lifecycle investing: use moderate leverage (1.5-2x) when young and reduce as your portfolio grows, aiming for consistent lifetime market exposure.

- 3.Don't become too conservative too early — a 60-year-old may have a 30-year time horizon, and excessive bonds lose to inflation.

This content is for educational purposes only and does not constitute investment advice. Trading and investing involve substantial risk of loss. Past performance is not indicative of future results. Always do your own research and consider seeking professional guidance before making financial decisions.