Imagine you could control £20,000 worth of stock for £6,000. If the stock goes up 20%, you make the same profit as the full-position investor. If it goes down 50%, you lose your £6,000 — but the full-position investor loses £10,000. And the £14,000 you didn't tie up? It's been earning interest or deployed in other investments.

This chapter is about one specific use of options: replacing stock positions with long-term options to get the same upside exposure at a fraction of the capital cost. We're not covering complex multi-leg strategies or exotic payoffs. One technique. One use case. Done right, it's transformative.

LEAPS also connect directly to the lifecycle investing framework from the previous chapter. If you're a younger investor looking to increase your effective market exposure without using margin, LEAPS are one of the cleanest ways to do it — leverage at a known, capped cost, without margin calls.

Options in Plain English

A call option gives you the right — but not the obligation — to buy an asset at a specific price by a specific date. If the stock goes up, your call increases in value. If it doesn't, you lose what you paid. That's your maximum loss.

Every option has a strike price (the price you can buy at), an expiration date (when it expires), and a premium (what you pay for it).

If the jargon ever gets confusing: a call option is a bet that the price goes up, with a known maximum loss and potentially unlimited upside.

What LEAPS Are and Why They Matter

LEAPS stands for Long-Term Equity Anticipation Securities — options with 12–24 months or longer until expiration. Standard options might expire in weeks. LEAPS give your thesis time to play out.

Why does expiration matter? Because every day that passes, an option loses a tiny bit of value due to time decay. With short-dated options, this decay is brutal. With LEAPS, time decay is minimal in the early months — a 24-month option barely decays at all for the first 6–12 months.

LEAPS let you express high conviction with leverage, without the margin call risk that destroys overleveraged traders.

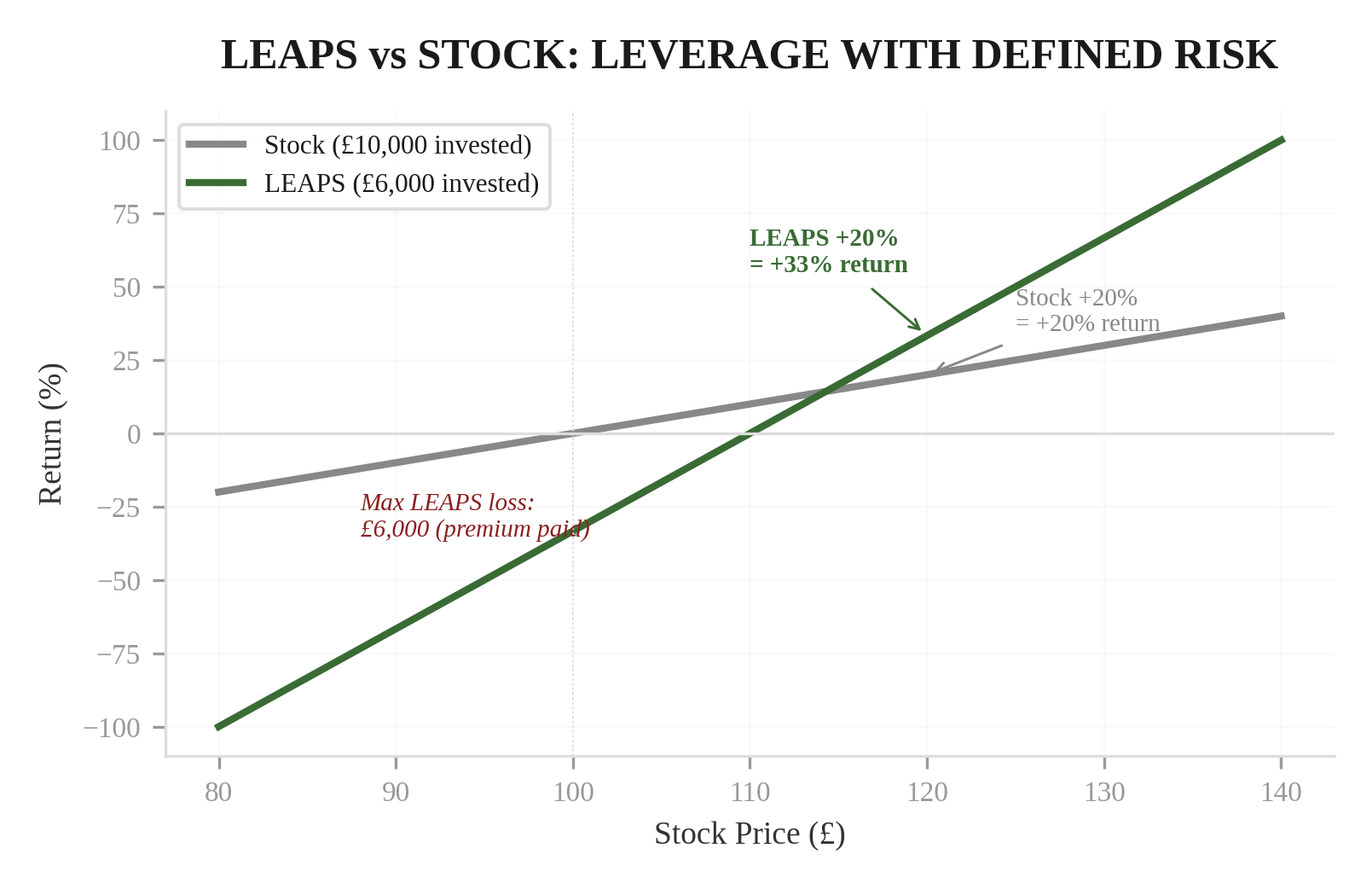

The Stock Replacement Strategy

Instead of buying 100 shares at £100 per share (£10,000), you buy one deep in-the-money call LEAP with a strike price well below the current stock price, expiring 18–24 months out. The option might cost £30–40 per share (£3,000–4,000 for 100 shares of exposure). You control the same number of shares for 30–40% of the capital.

The key: choose options that are deep in the money, with a delta of 0.80 or higher. Delta measures how much the option moves per £1 move in the stock. A delta of 0.85 means you get 85% of the stock's movement for 35% of the capital.

Worked Example: Stock Replacement with LEAPS

A large tech company at £180. Regime 1, strong uptrend, Grade A long-term opportunity.

| Scenario | Stock (£18,000) | LEAPS (£5,000) | Winner |

|---|---|---|---|

| Stock rises to £220 (+22%) | +£4,000 (+22%) | +£3,200 (+64%) | LEAPS (3x return %) |

| Stock flat at £180 | £0 | −£1,000 (−20%) | Stock (no time decay) |

| Stock falls to £140 (−22%) | −£4,000 | −£4,500 | Similar loss |

| Stock falls to £100 (−44%) | −£8,000 | −£5,000 (max) | LEAPS (capped loss) |

| Stock falls to £0 (−100%) | −£18,000 | −£5,000 (max) | LEAPS (capped loss) |

The LEAP outperforms on the upside, caps your loss on catastrophic declines, and frees £13,000 of capital for other investments. The trade-off? You lose money faster on moderate declines, and time decay eats into your position even if the stock doesn't move. Amplified upside, capped downside, a cost for the privilege.

The Rules for LEAPS

No spreads. No straddles. No iron condors. No multi-leg strategies. Those are tools for options traders, not investors using options as a leverage tool.

Always buy LEAPS with at least 18 months remaining. This minimises time decay in the early months. When 3–6 months remain, roll — sell the existing option and buy a new one with 18+ months.

Strike price well below current stock price. Look for delta of 0.80+. The deeper in the money, the more the option behaves like the stock (higher delta) and the less time value premium you pay.

LEAPS amplify both gains and losses. Only use them where macro, fundamentals, and price action all align. If conviction is below Grade A, buy the stock instead. Our market products grade every trade from A to E so you always know your conviction level.

If you'd normally allocate £18,000 to a position, spend £5,000–8,000 on LEAPS and deploy the remainder in uncorrelated investments, bonds, or cash. Don't put the freed-up capital into more LEAPS.

Understanding the Risks

100% premium loss possible. If the stock drops below your strike and stays there until expiration, the option expires worthless. You lose everything you paid. With shares, a 20% drop costs you 20%. With LEAPS, a 20% stock drop might cost you 50–60% of the premium.

Time decay is real. Even if the stock goes nowhere, your option loses value every day. A stock that finishes where it started costs you the entire time value portion of the premium.

Leverage amplifies everything. A 10% stock decline means a 25–30% decline in your LEAPS position. The amplification goes both ways. If you're not prepared for the volatility, LEAPS will shake you out at exactly the wrong moment.

Liquidity can be thin. Some LEAPS trade with wide bid-ask spreads. Always use limit orders. Check open interest — if it's below a few hundred, the liquidity isn't adequate for efficient execution.

Discovered LEAPS, got excited, and immediately replaced all five long-term positions with LEAPS on the same day. Six weeks later, the market corrected 12%. His stock positions would have been down 12%. His all-LEAPS portfolio was down 35%.

He panicked and sold everything at the bottom. Two months later, the market had fully recovered. His stock-holding friends were back to even. He'd locked in a 35% loss that didn't need to happen.

The lesson: Don't go all-in on LEAPS. Use them selectively — on your highest-conviction positions — as part of a portfolio that also includes standard stock positions, bonds, and cash.

With stocks, a 10% pullback feels manageable. With LEAPS, that same pullback shows as 25–30%. Three consecutive days of amplified losses and your rational brain has left the building entirely.

You start doing the maths: "If it drops another 5%, I'll be down 45%. Maybe I should cut now." That impulse is the entire risk of LEAPS. The numbers will try to scare you out of positions that, given time, would have been profitable. If you can't handle that amplified volatility without selling, LEAPS are not for you.

Calculating Your Leverage Cost

Every form of leverage has a cost. With LEAPS, the cost is the time value premium you pay above the option's intrinsic value.

Time value = Total premium − Intrinsic value

In our example: option costs £50, intrinsic value is £40 (stock at £180 minus £140 strike), so time value is £10. Use our free calculators to run these numbers for your own positions.

Over 20 months, you're paying £10 for the leverage — approximately £0.50/month per share, or about 3.3% annualised on the £180 stock price. Compare this to margin interest of 5–8% at most brokers. LEAPS leverage is often cheaper.

The next chapter covers how to build a complete portfolio that combines active trading, long-term investing, and options into a unified, regime-aware structure.

- 1.LEAPS let you control £20,000 of stock for £5,000-8,000, with amplified upside and capped downside at the premium paid.

- 2.Only use LEAPS on Grade A positions with 18+ months to expiration and delta of 0.80 or higher.

- 3.Don't go all-in on LEAPS — use them selectively as part of a portfolio that also includes standard positions and cash.

This content is for educational purposes only and does not constitute investment advice. Trading and investing involve substantial risk of loss. Past performance is not indicative of future results. Always do your own research and consider seeking professional guidance before making financial decisions.