Investing psychology is a different animal from trading psychology. Trading is about managing intensity — sharp emotional spikes compressed into hours. Investing is about managing duration — the slow, grinding test of patience that plays out over years and decades.

Most people fail at long-term investing not because they pick the wrong assets. They fail because they can't sit still. They can't endure the boredom. They can't resist the urge to "do something" when headlines are screaming. And they can't hold through the drawdowns that are an inevitable, necessary feature of every market that delivers long-term returns.

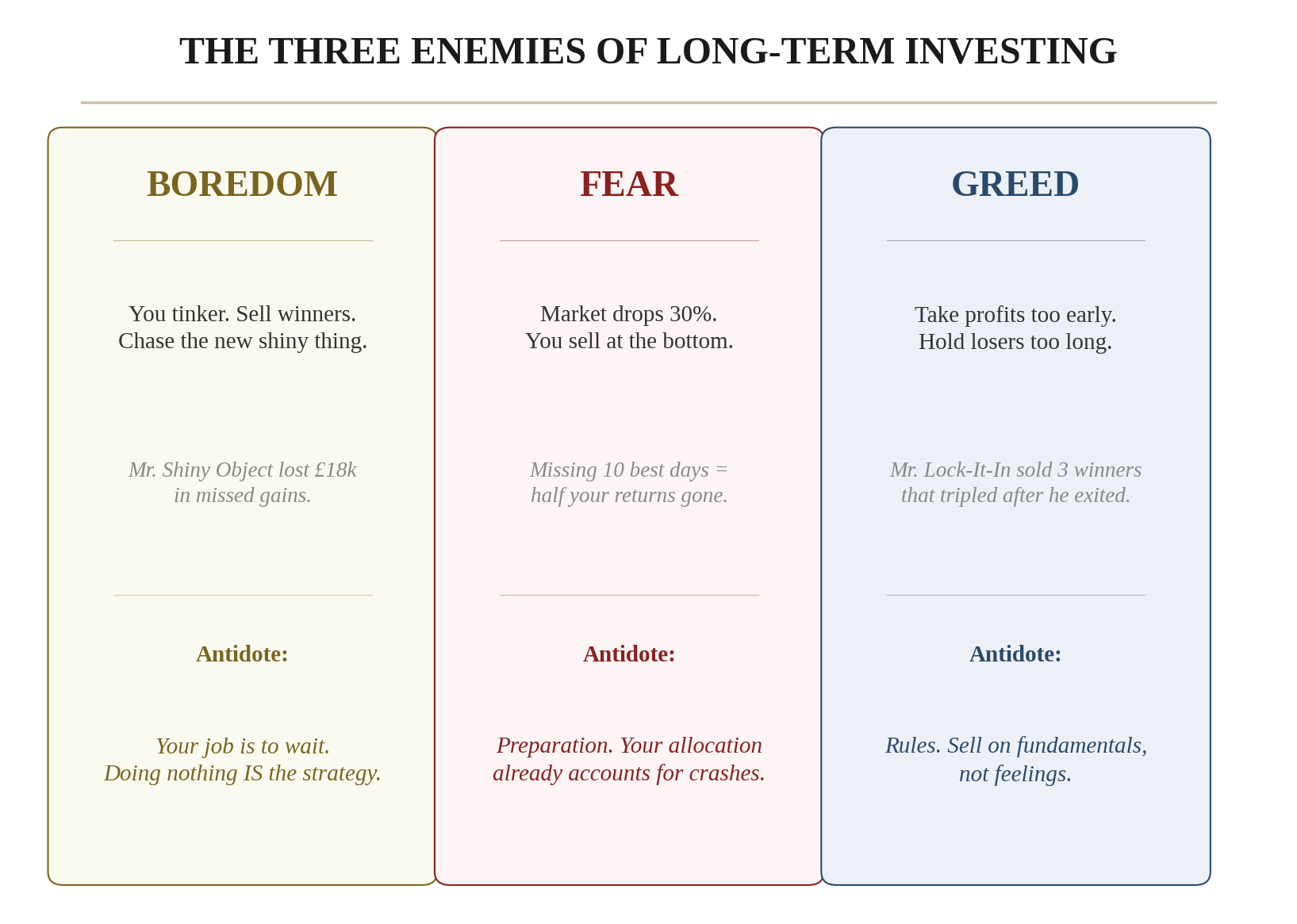

The Three Enemies

Enemy 1: Boredom

Long-term investing is, by design, boring. You buy quality assets in uptrends with macro support. You hold. You check quarterly. You rebalance annually. Months pass where the most productive thing you can do is nothing.

This drives people crazy. We are wired for action. We want to feel like we're "managing" our money. So we tinker. We sell a position that's "not doing anything." We check our portfolio daily, then hourly, then obsessively.

Had a near-perfect long-term portfolio. Five positions, all Grade A, all in uptrends, strong fundamentals. Lifecycle allocation right for his age. Costs minimal. Compounding beautifully.

Then he got bored. Over six months, he sold three positions to buy "more exciting" opportunities he'd read about on social media. The three positions he sold went on to gain a combined 47% over the following year. The "exciting" replacements averaged −8%. Boredom cost him £11,000 in missed gains.

Enemy 2: Fear

Markets drop 10–20% with regularity. They drop 30–50% roughly once a decade. This is not a bug. This is a feature. If markets didn't drop, there would be no risk premium, and stocks would deliver the same returns as a savings account.

But knowing this intellectually and experiencing it emotionally are entirely different things. When your portfolio drops 35% in six weeks, something primal takes over. Your brain screams: "Get out. Sell everything. Stop the pain."

Missing the ten best days in the market over a twenty-year period cuts your total return roughly in half. And those best days happen almost always during or immediately after crashes — the exact moments when most people have already sold.

I watched what happened in March 2020. The market dropped 34% in five weeks. Intelligent, experienced investors sold everything. "The economy is shutting down. This time is different." Things got clearer about three weeks later, when the market began a rally that would exceed all-time highs within five months. By the time the sellers felt safe buying back, they'd missed a 30–50% recovery.

Enemy 3: Greed

Greed doesn't feel like greed when you're experiencing it. It feels like intelligence. "I'm not being greedy — I'm recognising an opportunity." But when you find yourself overweighting a single position because it's been running, or abandoning your lifecycle allocation because stocks have been going up — that's greed wearing the mask of intelligence.

The most destructive form: selling winners too early and holding losers too long. The disposition effect — one of the most well-documented biases in behavioural finance.

Retired engineer, sharp mind. Bought five positions in 2019. Over two years, three went up significantly (40–110%) and two went down (−15% to −35%).

He sold all three winners. His reasoning: "I've made good money, let me lock it in." He kept both losers. "They'll come back." They didn't. One fell another 25%. His winning stocks — the ones he sold — continued climbing. One tripled after he exited.

He sold his flowers and watered his weeds.

A landmark study of over 10,000 individual investor accounts found that the stocks they sold subsequently outperformed the stocks they continued to hold by an average of 3.4% over the following year. They were selling their best ideas and keeping their worst ones — consistently, systematically, year after year.

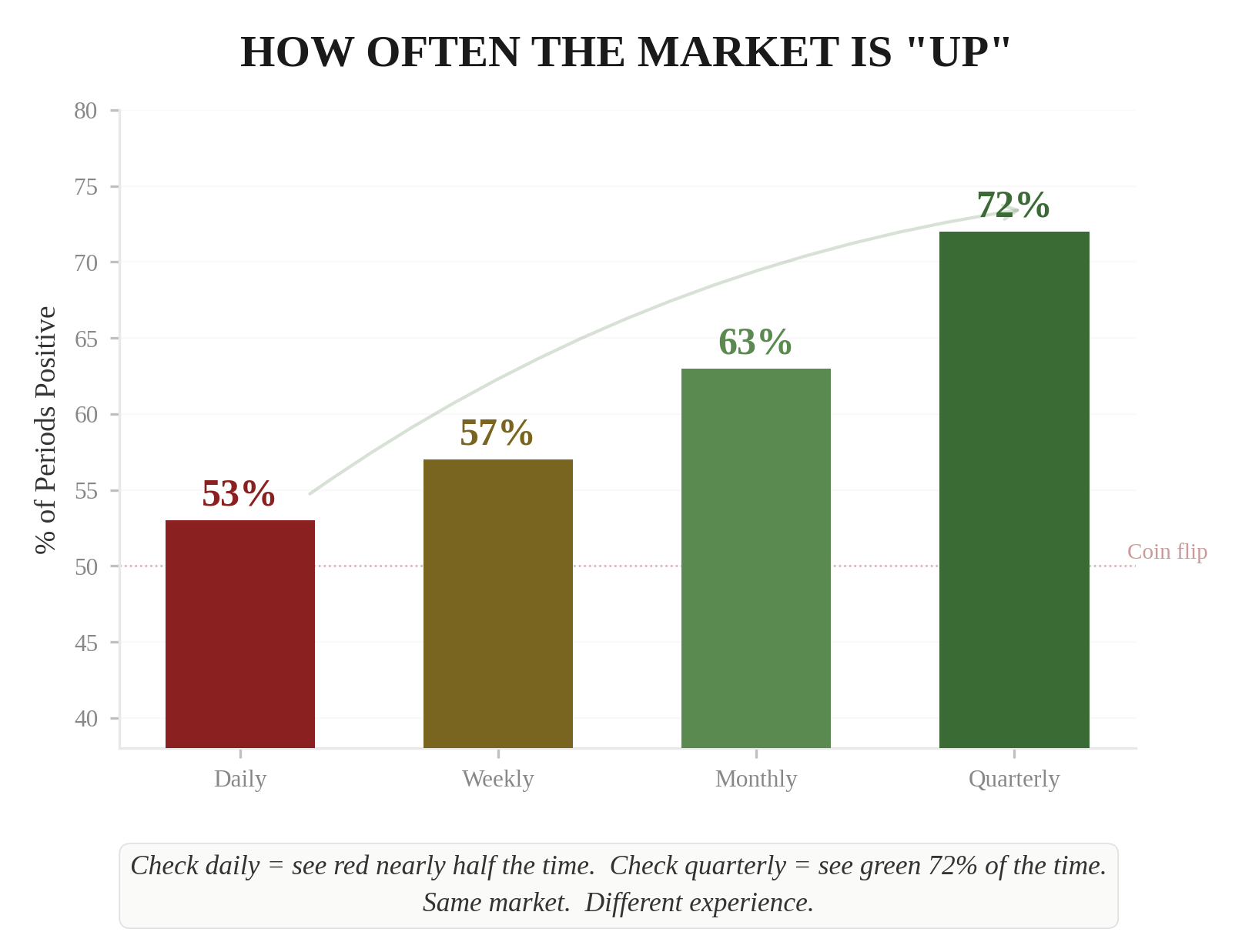

The Checking Frequency Problem

The stock market goes up on roughly 53% of trading days. That means on any given day, there's nearly a coin-flip chance you'll see red. Over a month, the odds improve to about 60% positive. Over a year, roughly 73%. Over ten years, historically close to 95%.

If you check daily, you're exposing yourself to negative noise almost half the time. If you check quarterly, you see positive returns roughly 70% of the time. Same portfolio. Same performance. different emotional experience.

Investors who check daily are significantly more likely to reduce risk exposure and sell during corrections. Daily checking makes you twice as likely to make the worst possible decision. To revisit these principles whenever you need grounding, download the full PDF and keep it handy.

Check quarterly. Set a calendar reminder four times a year. Review your positions, check the macro regime, confirm your allocation, and close the app. Your money grows better when you're not watching it.

The Compounding Illusion

Compounding is the most powerful force in investing, but it has a perverse quality: it's almost invisible in the early years and overwhelming in the later years. This creates a psychological trap.

In years 1–5, your portfolio barely moves. You're contributing £500 a month and your investment returns are adding maybe £2,000–3,000 a year. It feels pointless. People quit at this stage.

In years 5–15, the returns start to catch up to the contributions. You cross the tipping point where your money is making more than you're contributing. This is where conviction builds.

In years 15–30, the returns absolutely dwarf the contributions. The portfolio is doubling every 6–8 years. A single good year might add more to your wealth than five years of salary. But you only get here if you didn't quit in the first five years.

Person A gets frustrated after three years because his portfolio is only £22,000 and the returns feel like pocket change. He stops contributing but leaves the money invested. Person B keeps going.

At age 65: Person A has £340,000. Person B has £1,150,000. Three years of frustration cost Person A £810,000.

The early years are the hardest psychologically because they're the least rewarding financially. But they're the most important, because every pound invested in years 1–5 has the most time to compound.

What to Do When You're Tempted to Act

When the urge to "do something" strikes — and it will, repeatedly, for decades — run through this checklist before touching your portfolio:

Has my macro regime changed? If not, no action needed.

Have the fundamentals of any holdings deteriorated? If not, no action needed.

Has the long-term trend of any holdings broken? If not, no action needed.

Has my grade on any holding dropped? If not, no action needed. (Our trades update grades daily — try it free for 7 days.)

Am I feeling an emotion (fear, boredom, excitement, regret)? If yes, that's the emotion talking, not the data. Close the app. Come back in a week.

If you ran through all five questions and the answer to every one is "no," the correct action is no action. The most powerful move in long-term investing is often doing nothing at all.

The next chapter covers the platforms, tools, and technology stack that brings everything in this book together into a working system.

- 1.The three enemies of long-term investing are boredom (tinkering with a working portfolio), fear (selling during crashes), and greed (selling winners too early).

- 2.Check your portfolio quarterly, not daily — daily checking exposes you to negative noise 47% of the time and doubles your chance of panic-selling.

- 3.The early years of compounding feel pointless, but they're the most important — quitting in year 3 can cost you £810,000 by retirement.

This content is for educational purposes only and does not constitute investment advice. Trading and investing involve substantial risk of loss. Past performance is not indicative of future results. Always do your own research and consider seeking professional guidance before making financial decisions.